Blog

Recent Updates

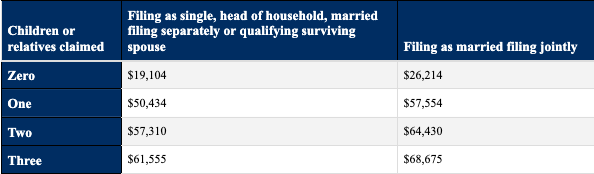

Understanding the 2025 Earned Income Credit (EIC)

Find out if you are eligible for the Earned Income Credit for low income earners. This is a refundable credit that our government funds for citizens with below average income. If you work minimum wage or part time you may be eligible for this credit.

Find the maximum AGI, investment income and credit amounts for tax year 2025.

moreIndividual Retirement Accounts (IRS.gov)

Planning for retirement may seem daunting, but it’s important to start early. Individual retirement accounts provide tax incentives for people to make investments towards their financial future.

IRAs let earnings grow tax deferred. Individuals pay taxes on investment gains only when they make withdrawals. Depositors may be able to claim a deduction on their individual federal income tax return for the amount they contributed to an IRA.

Here are some highlights for the many types of IRAs:

Traditional IRA

- Most common type of IRA and generally, the money in a traditional IRA isn't taxed until it's withdrawn

- There are annual limits to contributions depending on the person's age and the type of IRA

- When planning when to withdraw money from an IRA, taxpayers should know:

- They may face a 10% penalty and a tax bill if they withdraw money before age 59½, unless they qualify for an exception

- Usually, they must start taking withdrawals from the IRA when they reach age 73, age 72 if they turned 72 in 2022. For tax years 2019 and earlier, that age was 70½

- Special distribution rules apply for IRA beneficiaries

I am self-employed

TaxeaseUSA

If you are self-employed, you are responsible for paying both the employer and employee portions of Social Security and Medicare taxes, and you must make estimated tax payments quarterly. Unlike a traditional employee, you are your own bookkeeper, requiring you to track income and expenses to determine your taxable profit.

Self-employment tax

Tax rate: The total self-employment (SE) tax rate is 15.3%, which consists of 12.4% for Social Security and 2.9% for Medicare.

Net earnings: This 15.3% is applied to 92.35% of your net self-employment earnings, not your total revenue. The 92.35% figure is used because it is equivalent to deducting the 7.65% that an employer would normally pay for an employee.

Income cap: For 2025, the Social Security portion (12.4%) only applies to the first $176,100 of your combined wages and self-employment income. The Medicare portion (2.9%) has no income limit.

Estimated taxes

As a self-employed individual, you do not have an employer to withhold taxes from your paycheck, so the IRS requires you to make tax payments quarterly.

Payment schedule: Estimated taxes are typically due on April 15, June 15, September 15, and January 15 (of the following year).

moreI have multiple W2's

TaxeaseUSA

Why having more than one W-2 can lead to higher taxes

When you work multiple jobs during a tax year, you may end up with more than one W-2. This can affect your final tax liability in several ways:

1) Progressive tax rates and tax brackets

The U.S. federal income tax uses a progressive rate structure: portions of your taxable income are taxed at increasing rates.

If you add income from a second job, your total taxable income increases. Even though each employer withholds tax separately, the combined effect can push you into higher tax brackets or reduce the benefit of deductions and credits that phase out at higher income levels.

2) Withholding may be insufficient or inefficient

Each employer withholds based on the information you provide (usually via Form W-4). If you don’t adjust your W-4 withholdings after starting a second job, each employer might withhold only enough to cover their portion of your income, not your total tax liability.

Example: Job A withholds at a single filing status with standard deductions, and Job B does the same. Together, the withholdings may be too low to cover the total taxes owed on your combined income.

3) Standard deduction and phaseouts

more

Welcome

Welcome to our site! We are in the process of building our blog page and will have many interesting articles to share in the coming months. Please stay tuned to this page for information to come. And if you have any questions about our business or want to reach out to us, we would love for you to stop by our contact page.

Thank you!

more